Next: Propagation of Errors Up: StatisticTests Previous: Linear Regression

The null hypothesis for the linear regression model parameters is

the same as the hypothesized true value  and

and  .

If the residual

.

If the residual

is assumed to

be normally distributed with pdf

is assumed to

be normally distributed with pdf

, then the

estimated intercept and slope have normal pdfs:

, then the

estimated intercept and slope have normal pdfs:

(87)

(87)

(88)

(88)

and

and  are:

are:

(89)

(89)

(90)

(90)

is

is

(91)

(91)

degrees of freedom. Given a

significance level

degrees of freedom. Given a

significance level  , we can find either reject or accept

the null hypothesis that

, we can find either reject or accept

the null hypothesis that  .

.

Typically we assume  and test the null hypothesis

and test the null hypothesis

, i.e., there is no relationship between variables

, i.e., there is no relationship between variables

and

and  . The alternative hypothesis is

. The alternative hypothesis is

,

i.e., there is some relationship between and .

,

i.e., there is some relationship between and .

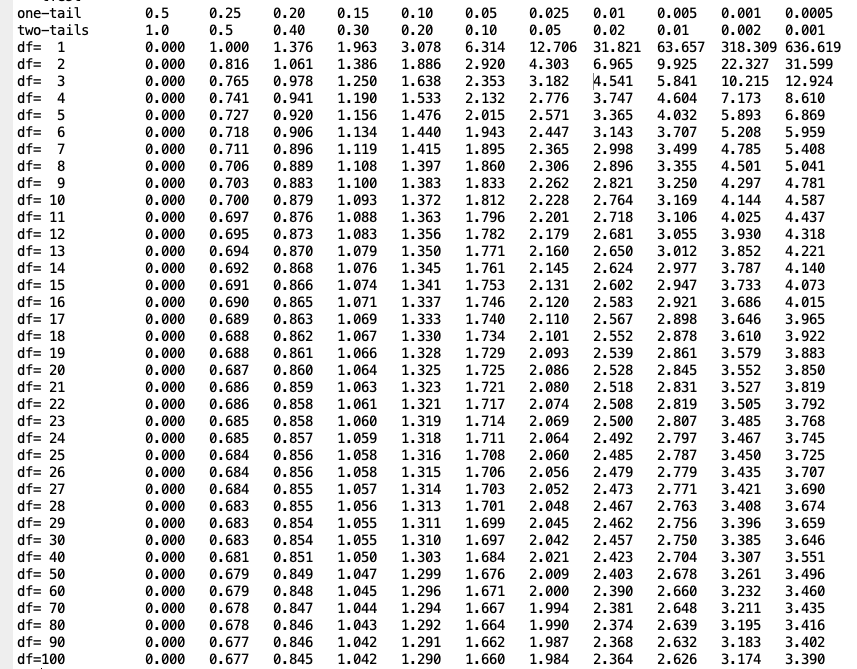

We can also find the upper and lower limits

from the t-table

(with ) so that

from the t-table

(with ) so that

(92)

(92)

|

|||

|

|

is

is

.

.

For multivariate linear regression, we can also carry out some

tests to answer questions such as which subset of the independent

variables

is most important in affecting

. For simplicity, we let

is most important in affecting

. For simplicity, we let

be a subset of

be a subset of

variables out of the

variables out of the  variables. Then the corresponding

null hypothesis

variables. Then the corresponding

null hypothesis

, i.e., variable is

not related to any variables in the subset

.

The corresponding test statistic is

, i.e., variable is

not related to any variables in the subset

.

The corresponding test statistic is

(93)

(93)

. This null hypothesis

can be either rejected or accepted depending on whether the p-value

is smaller than a pre-spedified significant level .

. This null hypothesis

can be either rejected or accepted depending on whether the p-value

is smaller than a pre-spedified significant level .

{kind=link}